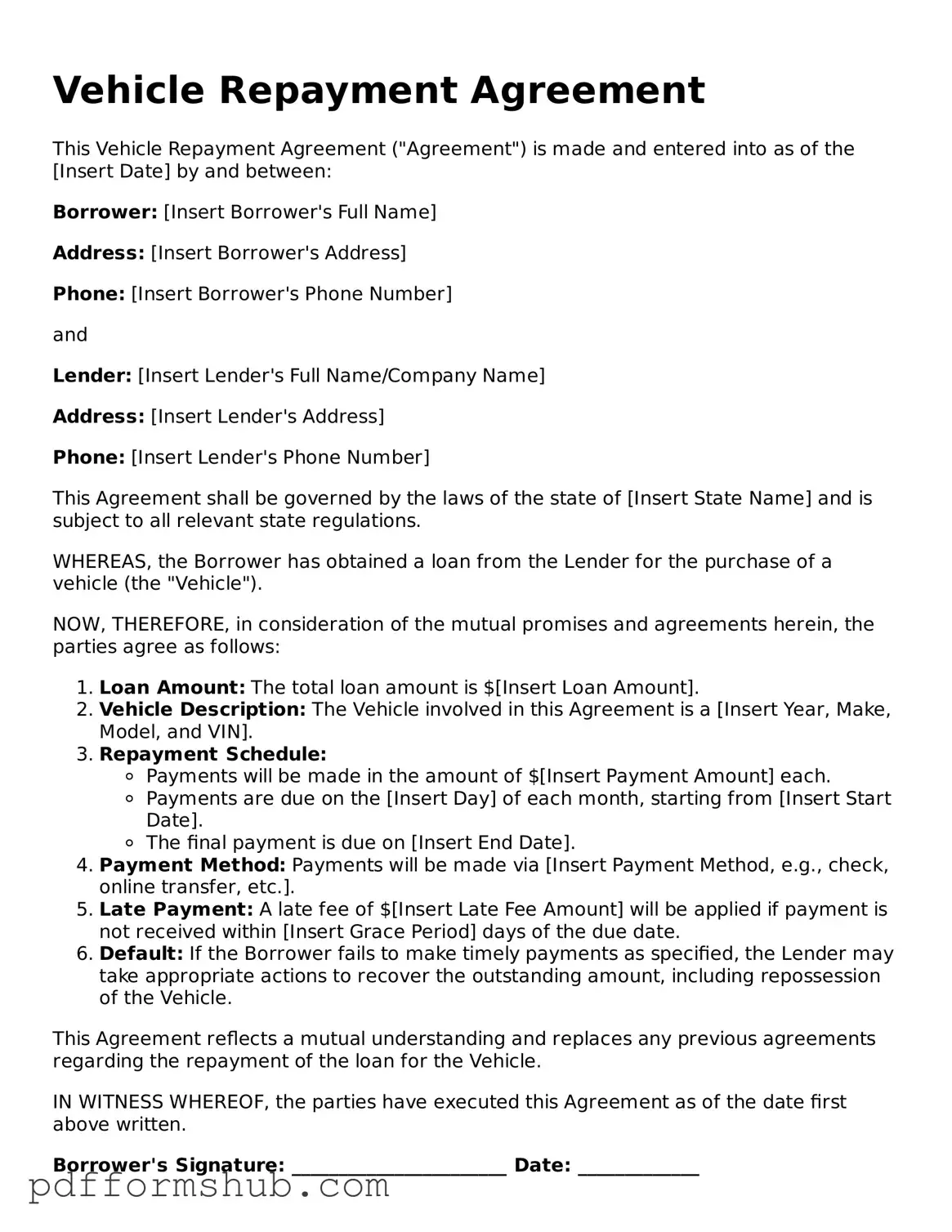

Valid Vehicle Repayment Agreement Form

PDF Forms Hub

Valid Vehicle Repayment Agreement Form

The Vehicle Repayment Agreement form is an essential document for individuals or entities involved in financing the purchase of a vehicle. This form outlines the terms and conditions under which the borrower agrees to repay the loan taken out to buy the vehicle. Key components of the agreement typically include the total amount financed, the interest rate, the repayment schedule, and any applicable fees. Additionally, it may specify the consequences of defaulting on the loan, such as repossession of the vehicle. Understanding these elements is crucial for both parties, as it helps ensure clarity and accountability throughout the repayment process. By signing this agreement, borrowers commit to fulfilling their financial obligations, while lenders gain a legal framework to protect their interests. It serves as a vital tool in the vehicle financing landscape, promoting transparency and mutual understanding between lenders and borrowers.

When entering into a Vehicle Repayment Agreement, several other forms and documents may be necessary to ensure a smooth process. Each document serves a specific purpose and helps clarify the terms of the agreement. Here are six commonly used documents:

Having these documents in order can help facilitate a successful Vehicle Repayment Agreement. Make sure to review each document carefully to avoid potential issues down the line.

When filling out the Vehicle Repayment Agreement form, it's essential to follow certain guidelines to ensure accuracy and compliance. Here are four things you should and shouldn't do:

What is a Vehicle Repayment Agreement?

A Vehicle Repayment Agreement is a legal document that outlines the terms under which a borrower agrees to repay a loan taken out for the purchase of a vehicle. This agreement typically includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

Who needs to sign the Vehicle Repayment Agreement?

Both the borrower and the lender must sign the Vehicle Repayment Agreement. The borrower is usually the individual or entity purchasing the vehicle, while the lender is typically a financial institution or dealership providing the loan. In some cases, a co-signer may also be required to sign if the borrower has limited credit history.

What happens if I miss a payment?

If a payment is missed, the lender may impose late fees as outlined in the agreement. Additionally, missed payments can negatively impact the borrower's credit score. In extreme cases, the lender may initiate repossession of the vehicle if the borrower defaults on the loan.

Can I modify the terms of the Vehicle Repayment Agreement?

Modifications to the Vehicle Repayment Agreement are possible, but they typically require mutual consent from both the borrower and the lender. Any changes should be documented in writing and signed by both parties to ensure clarity and legal enforceability.

What should I do if I cannot make a payment?

If you anticipate difficulty in making a payment, it is advisable to contact your lender as soon as possible. Many lenders offer options such as payment deferrals or restructuring of the loan. Open communication can help prevent further complications.

Is the Vehicle Repayment Agreement legally binding?

Yes, the Vehicle Repayment Agreement is a legally binding contract. Once signed by both parties, it creates enforceable obligations. It is important to read the agreement carefully and understand all terms before signing.

Progressive Supplement - This form enhances the accuracy of the services you'll receive.

Va Form 10 2850c - The VA 10-2850c includes sections for personal information, education, and professional experience.

When engaging in the sale of an ATV, it is vital to utilize a proper documentation process to ensure clarity and legality. The New York ATV Bill of Sale form provides a comprehensive method to record the transaction, confirming the swap of ownership between the seller and buyer. This form is not only a proof of purchase but also a necessary document for the registration of the ATV in the new owner's name. For further information and to download a template, visit https://nyforms.com/atv-bill-of-sale-template/.

Affidavit Death of Joint Tenant California - The affidavit is typically filed with the county recorder’s office where the property is located.

| Fact Name | Description |

|---|---|

| Definition | The Vehicle Repayment Agreement is a legal document outlining the terms under which a borrower agrees to repay a loan used to purchase a vehicle. |

| Governing Law | In many states, the agreement is governed by the Uniform Commercial Code (UCC) and specific state laws regarding secured transactions. |

| Parties Involved | The agreement typically involves two main parties: the lender (financial institution) and the borrower (vehicle purchaser). |

| Key Components | Essential components often include the loan amount, interest rate, repayment schedule, and consequences of default. |

| Signatures Required | Both parties must sign the agreement for it to be legally binding, indicating their acceptance of the terms. |

| Default Consequences | If the borrower fails to make payments, the lender may have the right to repossess the vehicle as outlined in the agreement. |