Valid Promissory Note Form

PDF Forms Hub

Valid Promissory Note Form

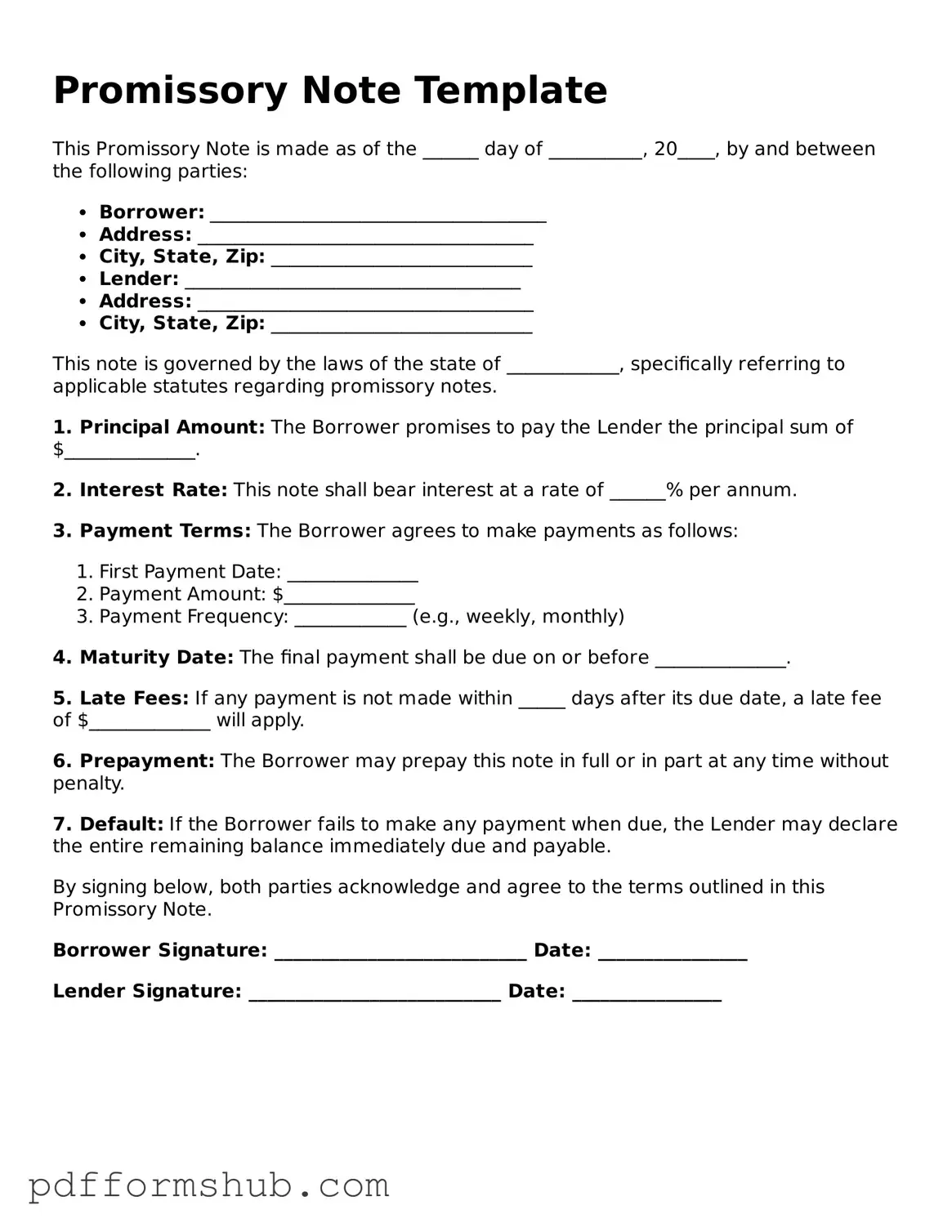

When it comes to lending and borrowing money, a Promissory Note serves as a crucial document that outlines the terms of the agreement between the lender and the borrower. This form typically includes essential details such as the principal amount, interest rate, repayment schedule, and any penalties for late payments. It acts as a written promise from the borrower to repay the loan under specified conditions, providing both parties with a clear understanding of their obligations. Additionally, a Promissory Note can be secured or unsecured, depending on whether the borrower offers collateral to back the loan. This flexibility makes it a popular choice for personal loans, business financing, and real estate transactions. By documenting the agreement in writing, the Promissory Note not only protects the lender’s interests but also helps the borrower maintain a record of their financial commitments. Understanding the components and implications of this form is essential for anyone involved in a loan agreement, ensuring that both parties are on the same page and reducing the likelihood of disputes down the road.

When entering into a loan agreement, a Promissory Note is often accompanied by several other important documents. These forms help clarify the terms of the agreement and protect the interests of all parties involved. Below is a list of common documents that are typically used alongside a Promissory Note.

Using these documents in conjunction with a Promissory Note can help ensure a clear understanding of the loan terms and protect the rights of both the lender and borrower. It is essential to review each document carefully and seek assistance if needed to ensure all parties are well-informed and protected.

When filling out a Promissory Note form, it’s important to follow certain guidelines to ensure the document is valid and clear. Here’s a list of things you should and shouldn’t do:

Following these guidelines will help create a clear and enforceable Promissory Note.

A promissory note is a written promise to pay a specific amount of money to a designated person or entity at a specified time or on demand. It serves as a legal document that outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payment.

Promissory notes are commonly used in various situations, such as personal loans between friends or family, business loans, and real estate transactions. Anyone who lends money or provides credit can use a promissory note to formalize the agreement.

A well-crafted promissory note should include:

Yes, a promissory note is a legally binding document. Once both parties sign it, they are obligated to adhere to the terms outlined in the note. If the borrower fails to repay the loan as agreed, the lender can take legal action to recover the owed amount.

Yes, a promissory note can be modified if both parties agree to the changes. It’s essential to document any modifications in writing and have both parties sign the revised note to ensure clarity and enforceability.

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They can pursue collection efforts, negotiate a new payment plan, or take legal action to recover the debt. The specific actions depend on the terms of the note and applicable laws.

While it's not legally required to have a lawyer draft a promissory note, it can be beneficial, especially for larger loans or complex agreements. A legal professional can help ensure that the note complies with state laws and adequately protects your interests.

1098 Mortgage - This form provides essential details about your mortgage account, including the servicer's contact information.

To simplify the process of completing the transfer of vehicle ownership, it is advisable to refer to reliable resources, such as the Templates and Guide, which provide helpful templates and instructions.

Notice of Rent Increase Template - This letter maintains a formal tone in financial communications.

How to Put a No Trespassing Order on Someone - A formal approach helps underscore the importance of property rights.

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a specified time or on demand. |

| Parties Involved | There are typically two parties in a promissory note: the maker (the person promising to pay) and the payee (the person receiving the payment). |

| Governing Law | Promissory notes are generally governed by the Uniform Commercial Code (UCC) in the United States, particularly Article 3. |

| Types of Notes | Promissory notes can be secured or unsecured. A secured note is backed by collateral, while an unsecured note is not. |

| Interest Rates | Promissory notes may include an interest rate, which specifies how much extra the borrower must pay back in addition to the principal. |

| State-Specific Forms | Some states have specific forms or requirements for promissory notes. For instance, California has its own guidelines under the California Civil Code. |

| Transferability | Promissory notes can often be transferred to another party through endorsement, allowing the new holder to collect the debt. |

| Default Consequences | If the maker fails to pay as promised, the payee has the right to take legal action to recover the owed amount. |

| Notarization | While notarization is not always required, having a promissory note notarized can provide additional legal protection and authenticity. |