Valid Promissory Note for a Car Form

PDF Forms Hub

Valid Promissory Note for a Car Form

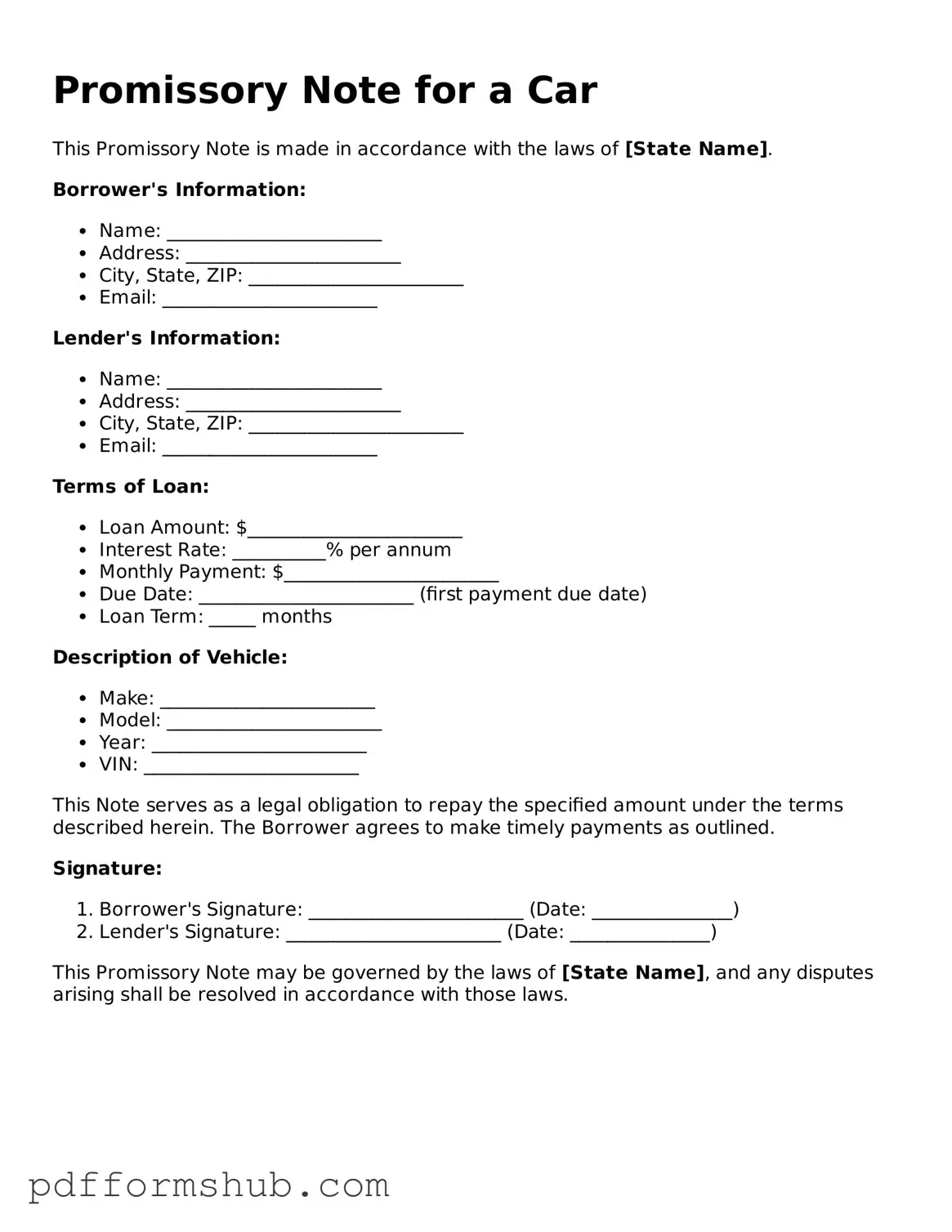

When purchasing a car, many buyers opt for financing options, which often involve the use of a promissory note. This legal document serves as a written promise to repay a loan under specific terms. It outlines critical information such as the loan amount, interest rate, repayment schedule, and any applicable fees. The promissory note also identifies the parties involved—the borrower and the lender—ensuring that both understand their rights and obligations. Additionally, it may include provisions for default, detailing the actions that can be taken if payments are not made on time. Understanding the nuances of this form is essential for both buyers and sellers, as it establishes the foundation for a financial agreement that can impact credit scores and ownership rights. By grasping the essential components of a promissory note for a car, individuals can navigate the financing process with greater confidence and clarity.

When financing a car, several documents work in tandem with the Promissory Note for a Car. Each document serves a specific purpose, ensuring that both the buyer and seller are protected throughout the transaction. Here’s a brief overview of these essential forms.

Understanding these documents can help facilitate a smoother car purchase process. Each plays a crucial role in protecting the interests of both the buyer and seller, ensuring a transparent and secure transaction.

When filling out the Promissory Note for a Car form, it’s important to approach the task with care and attention to detail. Here are some essential dos and don’ts to keep in mind:

By following these guidelines, you can help ensure that your Promissory Note is filled out correctly, making the process smoother for everyone involved.

What is a Promissory Note for a Car?

A Promissory Note for a Car is a written agreement between a borrower and a lender. In this document, the borrower promises to repay a specific amount of money borrowed for the purchase of a vehicle. It outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payments.

Who typically uses a Promissory Note for a Car?

This document is commonly used by individuals purchasing a car through financing. It can be utilized by private sellers, dealerships, or financial institutions. Both parties benefit from having a clear record of the loan terms and obligations.

What key information should be included in the Promissory Note?

Essential details to include are:

How is the interest rate determined?

The interest rate can vary based on several factors, including the borrower’s creditworthiness, the lender’s policies, and current market rates. It is important for borrowers to understand how the interest rate affects the total cost of the loan over time.

What happens if the borrower misses a payment?

If a payment is missed, the lender may impose a late fee as outlined in the Promissory Note. Repeated missed payments could lead to more severe consequences, including defaulting on the loan, which may result in repossession of the vehicle. Communication with the lender is crucial to avoid misunderstandings and to explore possible solutions.

Can the terms of the Promissory Note be modified?

Yes, the terms can be modified if both parties agree to the changes. It is advisable to document any amendments in writing to ensure clarity and protect both the borrower and lender. This helps to maintain a mutual understanding of the new terms.

Is a Promissory Note legally binding?

Yes, a Promissory Note is a legally binding document, provided it meets certain requirements, such as being signed by both parties. This means that both the borrower and lender are obligated to adhere to the terms outlined in the note. However, it is always wise to consult with a legal professional if there are any uncertainties regarding the implications of the agreement.

Satisfaction and Release Form - It helps prevent any future disputes regarding the note.

To create a comprehensive understanding of borrowing in New York, it is crucial to utilize a professional template for your agreements, such as the one available at https://nyforms.com/promissory-note-template/, which helps ensure all necessary terms and conditions are accurately captured in the promissory note. This approach aids in preventing potential disputes and upholds the legal integrity of the loan arrangement.

| Fact Name | Description |

|---|---|

| Definition | A promissory note for a car is a written promise to pay a specific amount of money for the purchase of a vehicle. |

| Parties Involved | Typically, the note involves two parties: the borrower (buyer) and the lender (seller or financial institution). |

| Legal Requirement | In most states, a promissory note is a legally binding contract that must be signed by both parties. |

| Interest Rates | The note may specify an interest rate, which is the cost of borrowing money over time. |

| Payment Schedule | It outlines a payment schedule, detailing when payments are due and how much is owed each time. |

| State-Specific Laws | Each state has its own laws governing promissory notes. For example, in California, the Uniform Commercial Code (UCC) applies. |

| Default Clause | The note may include a default clause, outlining what happens if the borrower fails to make payments. |

| Transferability | Promissory notes can often be transferred to another party, which means the lender can sell the note to someone else. |

| Secured vs. Unsecured | This type of note can be secured by the vehicle itself, meaning the lender can repossess the car if payments are not made. |

| Importance of Clarity | Clear terms and conditions in the note help prevent misunderstandings and disputes between the parties. |