Fill in Your Profit And Loss Form

PDF Forms Hub

Fill in Your Profit And Loss Form

Understanding the Profit and Loss form is essential for anyone managing a business, whether you're a seasoned entrepreneur or just starting out. This financial document provides a clear snapshot of a company's revenues, costs, and expenses over a specific period, typically a month, quarter, or year. By breaking down these elements, the form helps you assess how well your business is performing financially. You can identify trends in income and expenditures, which is crucial for making informed decisions about budgeting and future investments. Additionally, the Profit and Loss form can be a valuable tool for attracting investors or securing loans, as it illustrates your company's profitability and financial health. Overall, mastering this form will empower you to take control of your business's financial narrative.

The Profit and Loss form is a vital document for assessing a business's financial performance over a specific period. Alongside this form, several other documents can provide a more comprehensive view of the company's financial health. Below are four commonly used forms that complement the Profit and Loss statement.

In summary, the Profit and Loss form is just one piece of the financial puzzle. By reviewing these additional documents, stakeholders can gain a clearer understanding of the company's financial situation, aiding in informed decision-making.

When filling out the Profit and Loss form, keep these important points in mind:

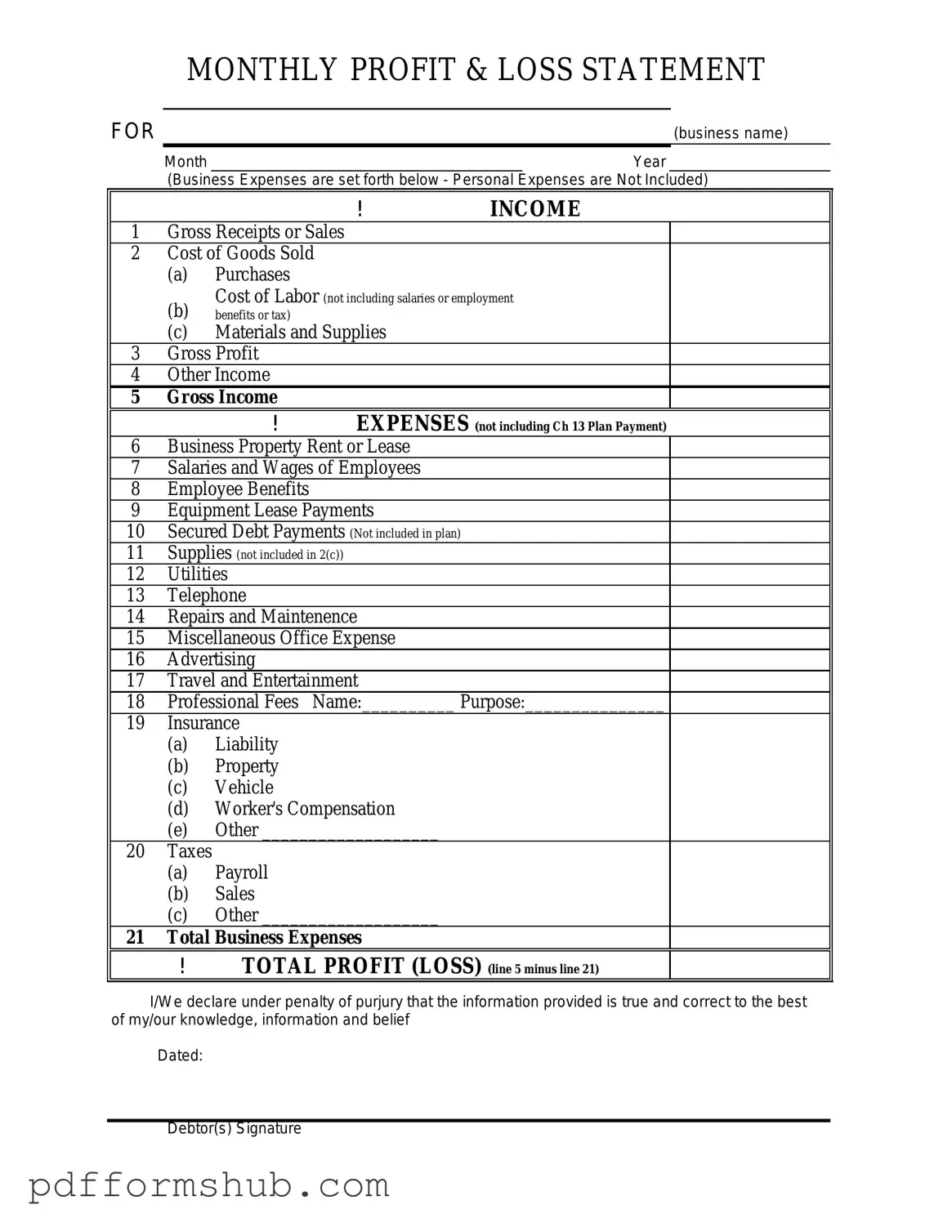

A Profit and Loss form, also known as an income statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period. This form helps businesses assess their financial performance by showing how much money was made or lost over that time frame.

The Profit and Loss form is crucial for several reasons. It provides insights into a company’s profitability, helps in identifying trends over time, and is often required for tax purposes. Additionally, it assists business owners and stakeholders in making informed decisions regarding budgeting and financial planning.

The form typically includes the following sections:

It is recommended that businesses prepare a Profit and Loss form on a regular basis. Many companies do this monthly, quarterly, or annually. Regular updates allow for better tracking of financial performance and enable timely adjustments to business strategies.

Yes, the Profit and Loss form can be a valuable tool for forecasting future financial performance. By analyzing past data, businesses can identify trends and make educated predictions about future revenues and expenses. This information is essential for setting realistic financial goals.

Creating a Profit and Loss form can be done using accounting software, spreadsheets, or templates available online. Begin by listing your revenue sources, then subtract COGS to find gross profit. Next, detail your operating expenses and subtract them from gross profit to arrive at net profit. Ensure that all figures are accurate and reflect the period in question.

Yugioh Deck List Form - Timeliness in submitting your deck list is appreciated.

2% Mindset - Assess your dining environment for improvements.

The importance of having a proper documentation cannot be overstated when purchasing an ATV, and that's where the ATV Bill of Sale form comes into play; it not only facilitates a smooth transaction but also protects both the buyer and the seller by recording all critical details of the sale.

Utility Bill Template Word - Ensure timely responses by filling out your preferred communication method.

| Fact Name | Description |

|---|---|

| Purpose | The Profit and Loss form summarizes a business's revenues and expenses over a specific period, helping to assess financial performance. |

| Components | It typically includes sections for gross income, operating expenses, and net profit or loss. |

| Frequency | Businesses usually prepare this form monthly, quarterly, or annually, depending on their reporting needs. |

| State-Specific Forms | Some states require specific formats or additional information, governed by local tax laws. |

| Governing Laws | For example, California's Profit and Loss form is governed by the California Revenue and Taxation Code. |

| Importance for Taxation | The information provided is crucial for preparing tax returns and ensuring compliance with federal and state tax laws. |

| Analysis Tool | It serves as an essential tool for business owners and stakeholders to analyze profitability and make informed decisions. |

| Comparative Analysis | By comparing multiple periods, businesses can identify trends and areas for improvement in their operations. |