Valid Loan Agreement Form

PDF Forms Hub

Valid Loan Agreement Form

When entering into a loan agreement, clarity and understanding are paramount for both the lender and the borrower. A well-structured loan agreement form serves as the foundation for this financial arrangement, outlining essential terms and conditions that govern the loan. Key components typically include the loan amount, interest rate, repayment schedule, and any collateral required. Additionally, the form addresses potential fees, default terms, and the rights of both parties in case of disputes. By carefully detailing these aspects, the loan agreement form not only protects the interests of the lender but also provides the borrower with a clear roadmap for repayment. Understanding the significance of each section ensures that both parties are aligned, fostering a transparent and trustworthy lending relationship.

When entering into a Loan Agreement, several other documents often accompany it to ensure clarity and protection for all parties involved. Each of these documents serves a specific purpose and helps to outline the terms and conditions of the loan more comprehensively.

Each of these documents plays a vital role in the loan process, helping to protect both the lender and the borrower. By understanding these accompanying forms, you can navigate the lending landscape with greater confidence and clarity.

When filling out a Loan Agreement form, attention to detail is crucial. Here are some essential dos and don'ts to consider:

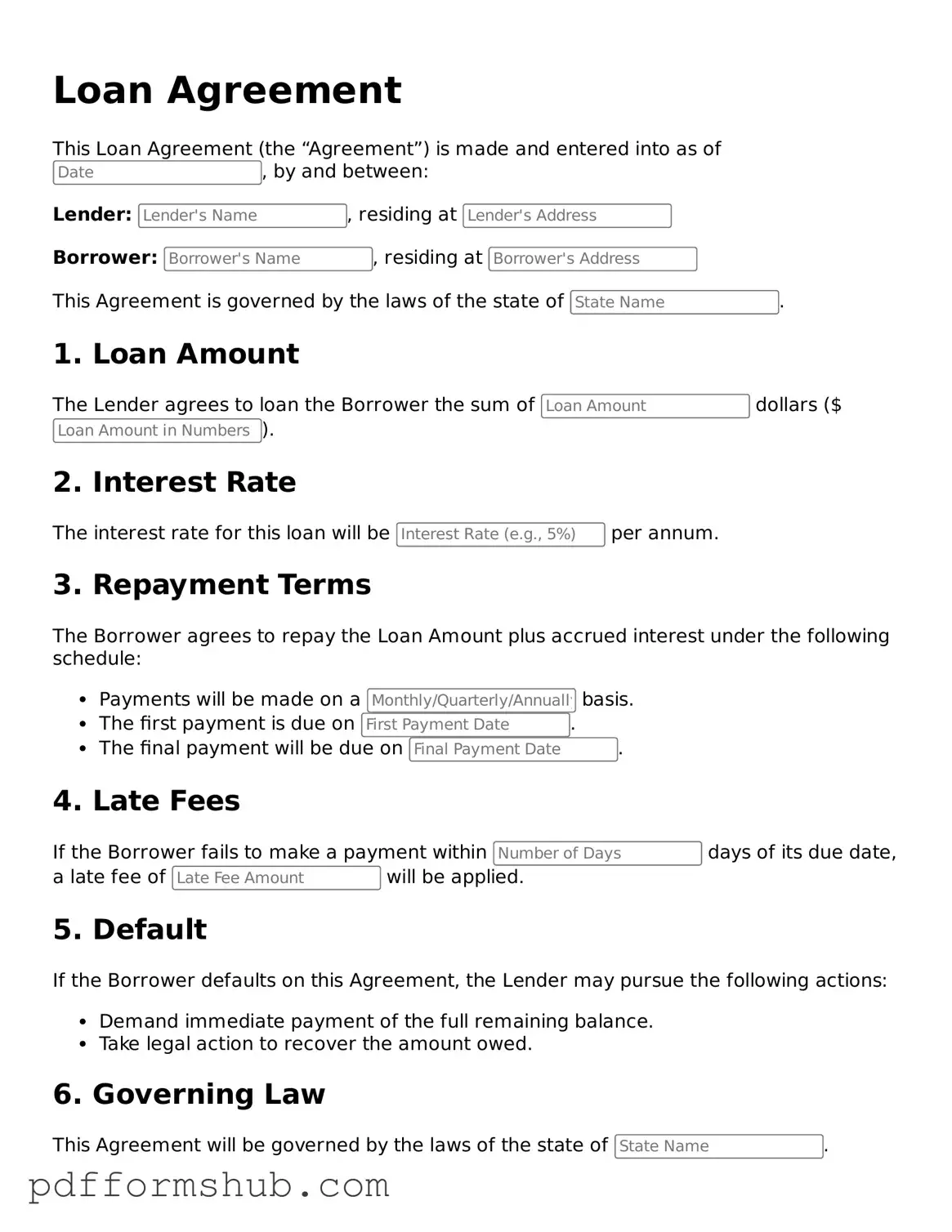

A Loan Agreement is a legal document that outlines the terms and conditions under which one party lends money to another. It details the amount borrowed, interest rates, repayment schedule, and any collateral involved. This document serves to protect both the lender and borrower by clearly defining their rights and responsibilities.

Anyone who is lending or borrowing money should consider using a Loan Agreement. This includes individuals, businesses, and financial institutions. Having a written agreement helps prevent misunderstandings and provides a clear record of the transaction.

A typical Loan Agreement includes:

Interest can be calculated in various ways, typically as a fixed rate or variable rate. A fixed rate remains constant throughout the loan term, while a variable rate may change based on market conditions. The Loan Agreement should specify how interest will be calculated and applied.

If the borrower defaults, the lender may take specific actions as outlined in the Loan Agreement. This could include charging late fees, accelerating the loan (demanding full repayment), or taking possession of any collateral. The agreement should clearly state the consequences of default.

Yes, a Loan Agreement can be modified if both parties agree to the changes. Modifications should be documented in writing and signed by both the lender and borrower to ensure clarity and enforceability.

Yes, a properly executed Loan Agreement is legally binding. Both parties must sign the document, and it should comply with applicable laws. This means that both the lender and borrower have legal recourse if the terms of the agreement are violated.

It is advisable to consult a lawyer, especially for larger loans or complex agreements. A legal professional can help ensure that the terms are fair and that your rights are protected. This step can prevent potential disputes in the future.

Proof of Service - A formal record of the service action taken in a court procedure.

Form I-9 - Provides insights into work ethic as observed during the employment period.

For those looking to streamline the process of transferring ownership, the New York ATV Bill of Sale form is an indispensable tool that clearly outlines the particulars of the transaction. By capturing essential details such as the buyer and seller's information, vehicle description, and sale price, this legal document plays a crucial role in ensuring clarity and transparency. For additional resources, you can refer to the Templates and Guide, which can aid you in this process and help you navigate any complexities involved.

Atv Bill of Sale Printable - Promotes trust and accountability in private sales.

| Fact Name | Description |

|---|---|

| Definition | A Loan Agreement is a legal document outlining the terms of a loan between a lender and a borrower. |

| Parties Involved | The agreement typically includes the lender (individual or institution) and the borrower (individual or business). |

| Loan Amount | The document specifies the total amount being borrowed, which is critical for clarity. |

| Interest Rate | The agreement outlines the interest rate, which can be fixed or variable, affecting repayment amounts. |

| Repayment Terms | It details the repayment schedule, including due dates and the duration of the loan. |

| Governing Law | The agreement will specify the state laws that govern the contract, which varies by location. |

| Default Conditions | It defines what constitutes a default and the consequences for the borrower in such an event. |

| Collateral | If applicable, the agreement may require collateral to secure the loan, reducing lender risk. |

| Amendments | The document should include provisions for amendments, allowing changes to be made with mutual consent. |