Attorney-Verified Deed in Lieu of Foreclosure Form for Illinois State

PDF Forms Hub

Attorney-Verified Deed in Lieu of Foreclosure Form for Illinois State

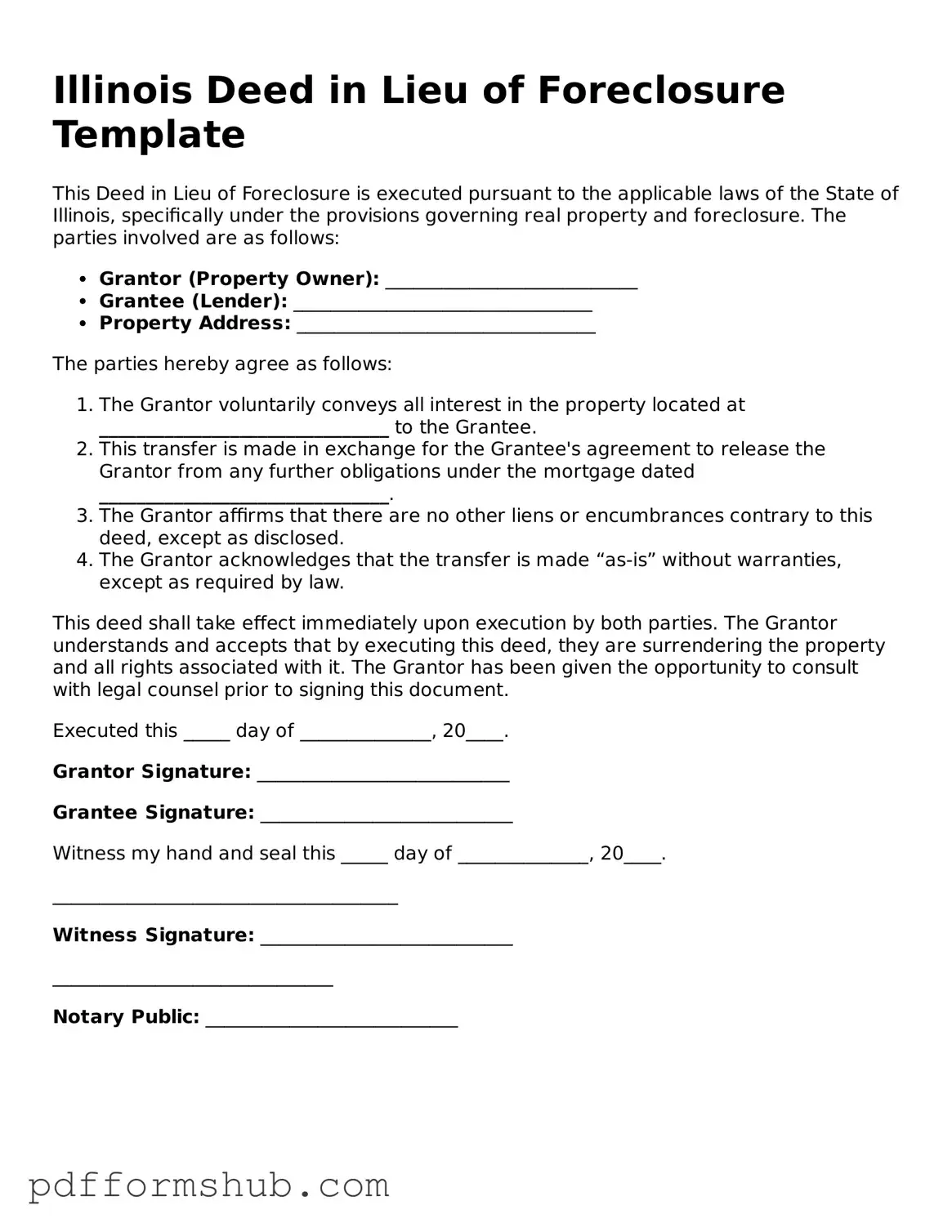

The Illinois Deed in Lieu of Foreclosure form serves as a critical tool for homeowners facing financial difficulties and potential foreclosure. This legal document allows a property owner to voluntarily transfer ownership of their property to the lender, thereby avoiding the lengthy and often costly foreclosure process. By executing this form, homeowners can mitigate the negative impact on their credit scores and potentially negotiate more favorable terms with their lenders. The form outlines the responsibilities of both parties, ensuring that the transfer is clear and legally binding. Furthermore, it includes important provisions regarding the condition of the property and any existing liens, which can affect the transaction's validity. Understanding the implications of this form is essential for homeowners seeking to protect their financial interests while navigating a challenging housing market.

When navigating the complexities of real estate transactions, especially those involving distressed properties, a Deed in Lieu of Foreclosure can be an essential tool. However, it often works in conjunction with several other important documents. Each of these documents plays a crucial role in ensuring that the process is smooth and legally sound.

Understanding these documents can significantly ease the stress of a Deed in Lieu of Foreclosure. Each plays a vital role in protecting the interests of both the borrower and lender, ensuring a fair and transparent process. By familiarizing yourself with these forms, you can navigate the complexities of real estate transactions with greater confidence.

When filling out the Illinois Deed in Lieu of Foreclosure form, it's essential to approach the process carefully. Here are some important do's and don'ts to keep in mind:

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer ownership of their property to the lender to avoid foreclosure. This process can help both the homeowner and the lender by simplifying the resolution of a defaulted mortgage.

In this arrangement, the homeowner agrees to hand over the property to the lender. In return, the lender typically agrees to forgive the remaining mortgage debt. This can help the homeowner avoid the lengthy and often stressful foreclosure process.

Homeowners facing financial hardship and unable to continue making mortgage payments may be eligible. Lenders usually require that the homeowner demonstrate their inability to pay and may review their financial situation. It's essential to communicate with the lender early in the process.

While there are benefits, there are also potential downsides. Homeowners may face tax implications if the lender forgives a portion of the debt. Additionally, not all lenders accept a Deed in Lieu of Foreclosure, and some may require the homeowner to exhaust other options first.

The process typically involves several steps. First, the homeowner must contact their lender to express interest in this option. Next, the lender will review the homeowner's financial situation. If approved, the homeowner will sign the deed, and the lender will take ownership of the property.

Generally, once the Deed in Lieu of Foreclosure is executed, the homeowner must vacate the property. However, some lenders may allow a grace period for the homeowner to find alternative housing. It’s important to discuss this with the lender early in the process.

Foreclosure Process in Georgia - Engaging a real estate attorney can provide valuable guidance throughout the deed in lieu process.

An Employment Verification Form is a document used by employers to confirm a candidate's employment history. This form typically requests information such as job titles, dates of employment, and salary details. To enhance the process of creating this form, many organizations rely on resources like Templates and Guide, which provide valuable templates and tips. Providing an accurate verification helps employers make informed hiring decisions.

| Fact Name | Details |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is a legal document where a borrower voluntarily transfers property ownership to the lender to avoid foreclosure. |

| Governing Law | The process is governed by the Illinois Compiled Statutes, specifically 735 ILCS 5/15-1402. |

| Requirements | The borrower must be in default on the mortgage, and the lender must agree to accept the deed. |

| Benefits | This option can help borrowers avoid the lengthy and costly foreclosure process and minimize damage to their credit score. |

| Risks | Borrowers may still be liable for any deficiency if the property's value is less than the mortgage balance, depending on the agreement with the lender. |