Attorney-Verified Promissory Note Form for Florida State

PDF Forms Hub

Attorney-Verified Promissory Note Form for Florida State

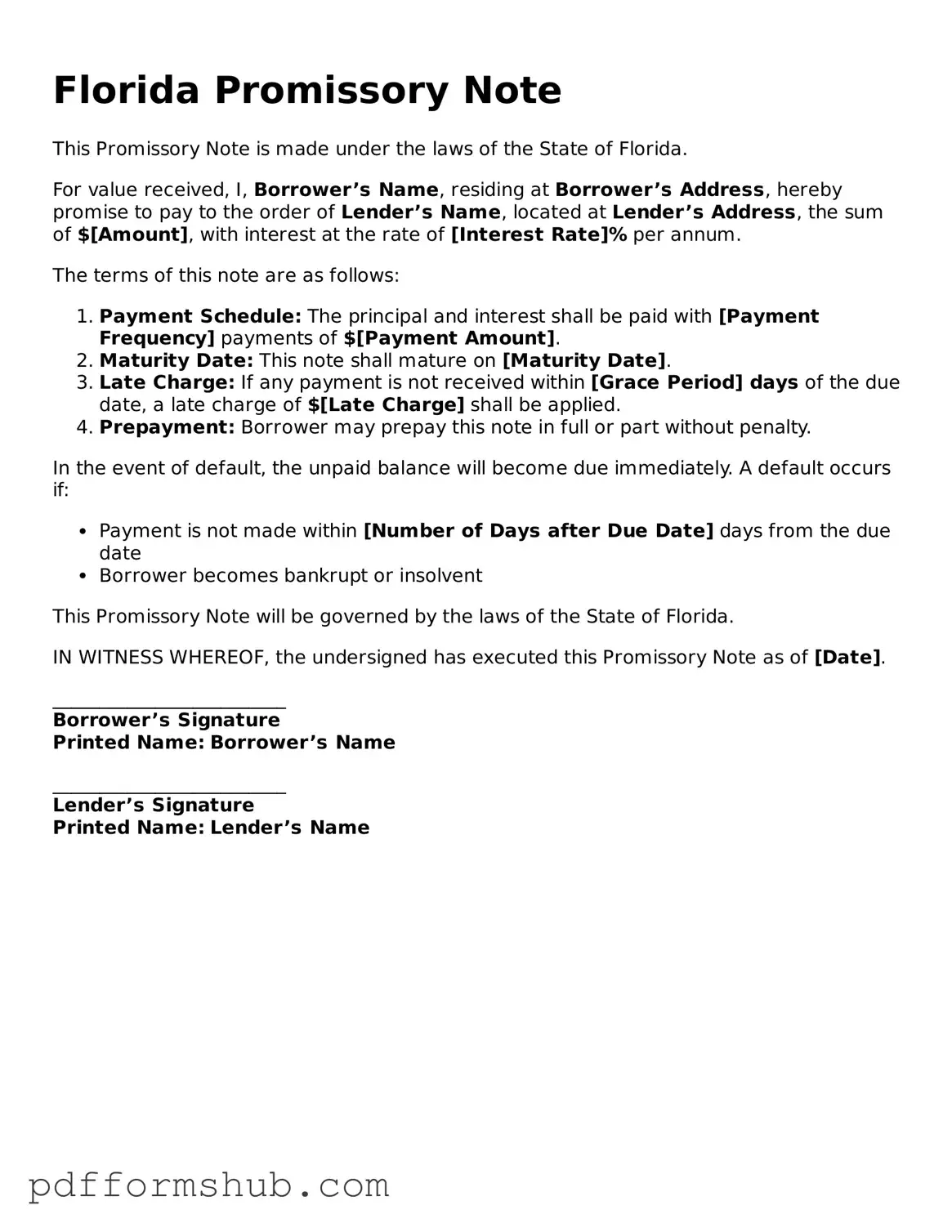

The Florida Promissory Note form serves as a crucial document in financial transactions, outlining the terms under which one party borrows money from another. This form typically includes essential details such as the principal amount, interest rate, repayment schedule, and any late fees that may apply. It also specifies whether the note is secured or unsecured, which can significantly impact the lender's rights in case of default. Additionally, the form may include provisions for prepayment, allowing the borrower to pay off the loan early without penalty. Understanding these components is vital for both lenders and borrowers to ensure that their rights and obligations are clearly defined. In Florida, specific legal requirements must be met for the promissory note to be enforceable, making it important for parties to use a properly formatted and compliant document. Overall, the Florida Promissory Note form plays a key role in establishing trust and clarity in lending agreements, protecting the interests of both parties involved.

When entering into a loan agreement, several documents may accompany the Florida Promissory Note. Each document serves a specific purpose and helps clarify the terms and conditions of the loan. Here is a list of commonly used forms and documents:

Understanding these documents can help borrowers and lenders navigate the loan process more effectively. Each plays a crucial role in establishing the rights and responsibilities of both parties, ensuring a clear and enforceable agreement.

When filling out the Florida Promissory Note form, it’s important to follow specific guidelines to ensure accuracy and compliance. Here are some things to do and avoid:

A Florida Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. This note specifies the amount borrowed, the interest rate, and the repayment schedule. It serves as a formal record of the debt and the terms agreed upon by both parties.

Any individual or business can use a Promissory Note in Florida. It is commonly used for personal loans, business loans, or real estate transactions. Both the borrower and lender must be of legal age and have the capacity to enter into a contract.

A comprehensive Promissory Note should include:

Yes, a properly executed Promissory Note is legally binding in Florida. It creates an enforceable obligation for the borrower to repay the loan under the terms specified. If the borrower fails to repay, the lender has the right to take legal action to recover the owed amount.

Yes, a Promissory Note can be modified if both parties agree to the changes. This may involve adjusting the repayment terms, interest rate, or other conditions. It is advisable to document any modifications in writing and have both parties sign the amended note.

If the borrower defaults, the lender may pursue various remedies. This could include demanding immediate payment of the full amount owed, charging late fees, or initiating legal proceedings to recover the debt. The specific actions taken will depend on the terms outlined in the Promissory Note.

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A lawyer can ensure that the note complies with Florida laws and adequately protects your interests. This is especially important for larger loans or complex agreements.

Yes, a Promissory Note is commonly used for business loans. It can help formalize the borrowing process between business partners or between a business and an individual lender. The terms should clearly outline the repayment structure and any interest rates applicable to the loan.

A Promissory Note should be signed by both the borrower and the lender. It is advisable to have the signatures witnessed or notarized to add an extra layer of authenticity. This can help prevent disputes about the validity of the document in the future.

Free Promissory Note Template California - These notes frequently contain a section for addressing late payment penalties or fees.

For those looking to understand the requirements for transferring ownership of an all-terrain vehicle, the document known as the ATV Bill of Sale essentials is crucial. This form not only serves as written proof of the transaction but also ensures that all legal obligations pertaining to the sale are fulfilled.

Illinois Promissory Note - A promissory note may be used alongside a more detailed loan agreement.

| Fact Name | Description |

|---|---|

| Definition | A Florida Promissory Note is a legal document in which one party promises to pay a specific amount of money to another party at a defined time. |

| Governing Law | Promissory Notes in Florida are governed by the Florida Uniform Commercial Code (UCC), specifically Chapter 673. |

| Parties Involved | The document involves two primary parties: the borrower (maker) and the lender (payee). |

| Interest Rate | The interest rate can be fixed or variable, and it should be clearly stated in the note. |

| Payment Terms | Payment terms, including the due date and any installment schedules, must be explicitly outlined. |

| Default Conditions | Conditions that trigger a default, such as late payments, should be included to protect the lender's rights. |

| Signatures | Both parties must sign the Promissory Note for it to be legally binding, ensuring mutual agreement. |