Attorney-Verified Deed in Lieu of Foreclosure Form for Florida State

PDF Forms Hub

Attorney-Verified Deed in Lieu of Foreclosure Form for Florida State

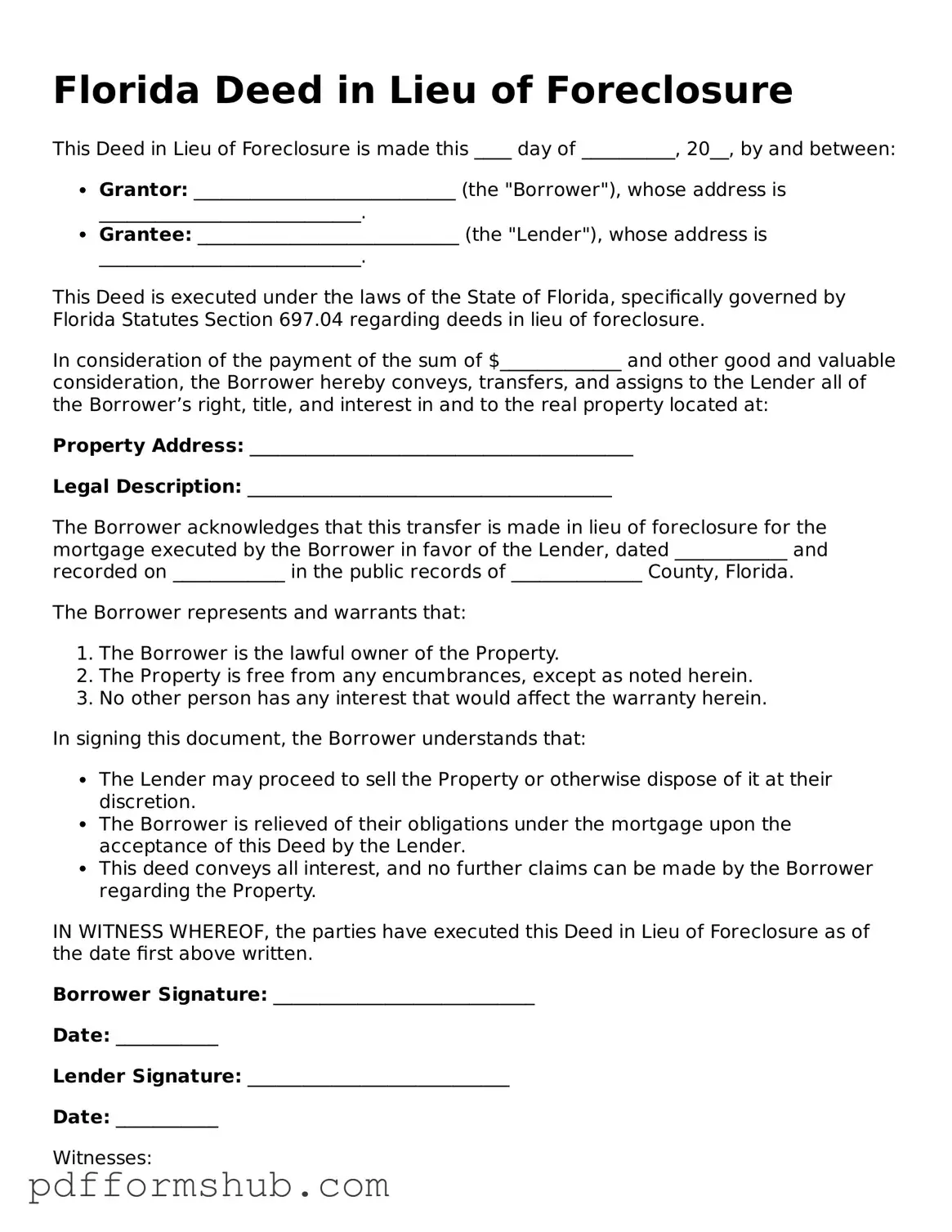

In the state of Florida, homeowners facing financial difficulties may find themselves considering various options to avoid foreclosure. One such option is the Deed in Lieu of Foreclosure, a legal process that allows a homeowner to voluntarily transfer ownership of their property to the lender. This arrangement can provide a more streamlined and less stressful alternative to the lengthy foreclosure process. By signing the Deed in Lieu of Foreclosure form, the homeowner relinquishes their rights to the property in exchange for the lender's agreement to cancel the mortgage debt. This form typically includes essential details such as the property description, the parties involved, and any relevant terms or conditions. Importantly, it can also outline the lender's commitment to release the homeowner from further liability, which can be a significant relief for those overwhelmed by debt. Understanding the implications and requirements of this form is crucial for homeowners seeking to navigate their financial challenges effectively.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer the title of their property to the lender to avoid foreclosure. This process often involves several other forms and documents to ensure a smooth transaction. Below is a list of common documents used alongside the Deed in Lieu of Foreclosure in Florida.

Each of these documents plays a vital role in the Deed in Lieu of Foreclosure process. They help clarify the terms of the transfer, protect the interests of both parties, and ensure compliance with legal requirements. Understanding these documents can facilitate a smoother transition for homeowners facing foreclosure.

When filling out the Florida Deed in Lieu of Foreclosure form, it is crucial to approach the process with care. Below are ten important guidelines to consider.

Following these guidelines can help ensure a smoother process and protect the interests of all parties involved.

A Deed in Lieu of Foreclosure is a legal agreement between a homeowner and their lender. In this arrangement, the homeowner voluntarily transfers the title of their property to the lender to avoid the foreclosure process. This option may be pursued when a homeowner is unable to keep up with mortgage payments and wishes to prevent the negative consequences associated with foreclosure.

There are several benefits to consider. First, it can help preserve the homeowner's credit score, as it may be less damaging than a foreclosure. Second, the process is often quicker and less costly than going through a full foreclosure. Additionally, homeowners may be able to negotiate a release from their mortgage debt, which can provide significant financial relief.

While there are benefits, it is important to acknowledge potential drawbacks. Homeowners may still face tax implications, as forgiven debt could be considered taxable income. Furthermore, not all lenders accept deeds in lieu of foreclosure, so homeowners may need to negotiate this option. Lastly, the homeowner will lose their property, which can be emotionally challenging.

The process typically begins with the homeowner contacting their lender to express interest in a Deed in Lieu of Foreclosure. The lender will evaluate the homeowner's financial situation and the property's value. If both parties agree, they will draft a deed that transfers ownership. The homeowner will then sign the deed, and the lender will record it with the county. This process can often be completed more swiftly than traditional foreclosure proceedings.

Homeowners should first consult with a qualified attorney or a housing counselor to fully understand the implications of a Deed in Lieu of Foreclosure. It is also wise to review their financial situation and explore all available options, including loan modifications or short sales. Gathering all relevant documents, such as mortgage statements and financial records, will help facilitate discussions with the lender.

The Loan Servicer Might Agree to Put the Foreclosure on Hold to Give You Some Time to Sell Your Home - The process can vary by state regulations and lender policies affecting eligibility and liabilities.

Understanding the importance of planning for your child's welfare is crucial, especially when you are unable to be there. The Florida Power of Attorney for a Child form serves as an essential tool in ensuring that trusted individuals can step in and make necessary decisions regarding your child's education, health, and overall well-being. For more detailed information and to access the form, you can visit floridaformspdf.com/printable-power-of-attorney-for-a-child-form/.

Foreclosure Process in Georgia - For homeowners at risk of foreclosure, a deed in lieu can provide a quick exit strategy from an untenable financial situation.

California Property Transfer Deed - Signing this deed can provide immediate relief from mortgage payments for homeowners in distress.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers ownership of their property to the lender to avoid foreclosure. |

| Governing Law | In Florida, the deed in lieu of foreclosure is governed by state statutes, particularly Florida Statutes Chapter 697. |

| Process | The borrower must request the deed in lieu and provide necessary documentation to the lender for approval. |

| Benefits | This option can help borrowers avoid the lengthy and costly foreclosure process, preserving their credit score to some extent. |

| Risks | Borrowers may still face tax implications, as forgiven debt can be considered taxable income. |

| Title Transfer | Upon execution of the deed, the lender receives full title to the property, and the borrower relinquishes all rights. |

| Impact on Credit | While a deed in lieu may be less damaging than foreclosure, it can still negatively impact a borrower's credit score. |

| Alternatives | Borrowers may consider alternatives such as loan modification, short sale, or bankruptcy before opting for a deed in lieu. |