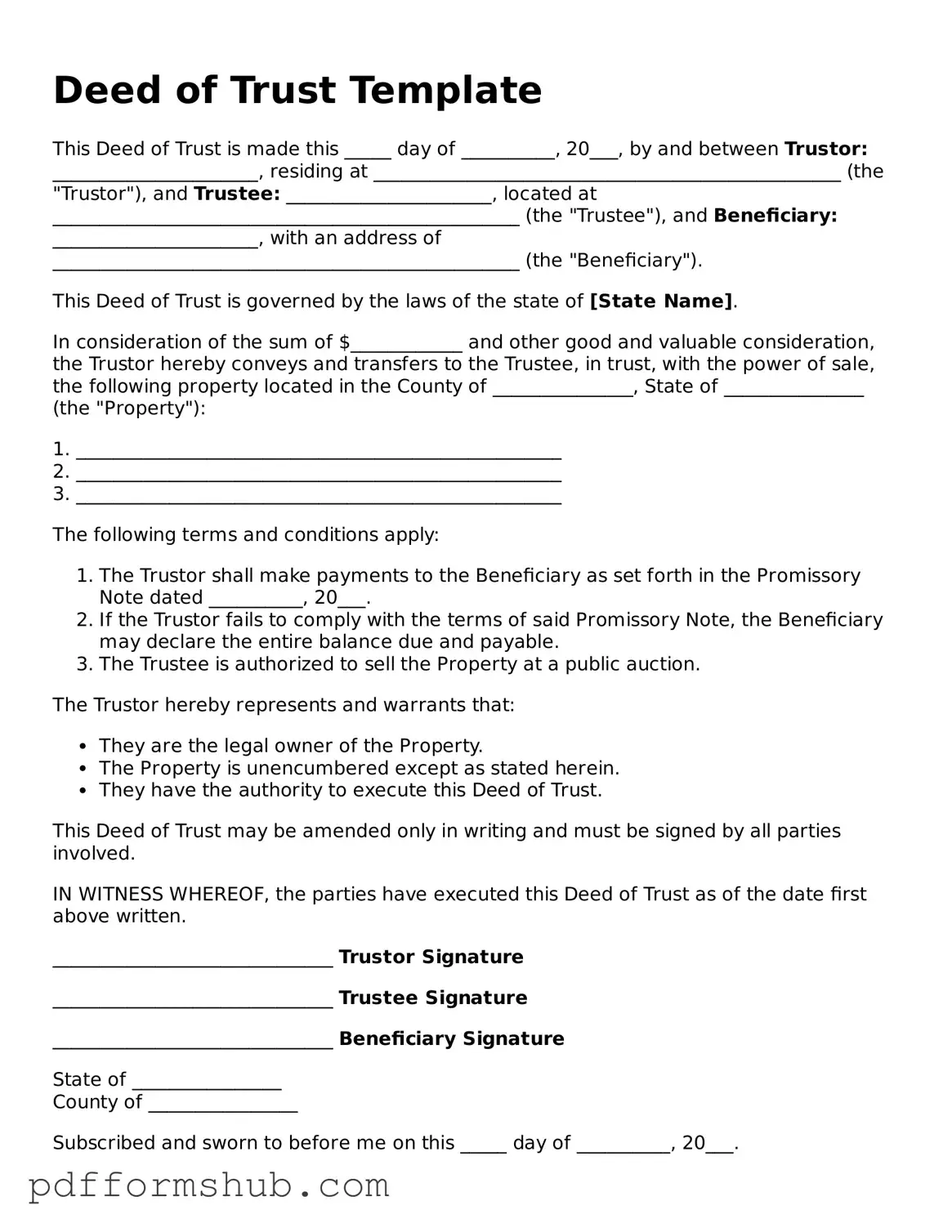

Valid Deed of Trust Form

PDF Forms Hub

Valid Deed of Trust Form

When it comes to securing a loan for purchasing real estate, understanding the Deed of Trust form is essential. This important document serves as a legal agreement between a borrower, a lender, and a third party known as a trustee. Essentially, it outlines the terms of the loan and establishes the rights and responsibilities of each party involved. The Deed of Trust not only details the amount borrowed and the interest rate but also specifies the property being financed and the repayment schedule. In the event of a default, this form provides a clear process for the lender to recover their investment, typically through a non-judicial foreclosure. Additionally, it includes provisions that protect both the borrower and the lender, ensuring that all parties understand their obligations. By grasping the key elements of the Deed of Trust, individuals can navigate the complexities of real estate transactions with greater confidence.

A Deed of Trust is a crucial document in real estate transactions, particularly when a borrower takes out a loan to purchase property. However, several other forms and documents often accompany it to ensure the process is clear and legally binding. Below is a list of these documents, each serving a specific purpose in the transaction.

Understanding these documents can help borrowers navigate the complexities of securing a loan. Each plays a vital role in protecting the interests of both the lender and the borrower throughout the transaction.

When filling out a Deed of Trust form, it is essential to approach the task with care and attention to detail. Here are some important guidelines to follow:

Following these guidelines can help ensure that the Deed of Trust is filled out correctly and serves its intended purpose effectively.

A Deed of Trust is a legal document that secures a loan by transferring the title of a property to a trustee. This document outlines the terms of the loan and the responsibilities of both the borrower and the lender. In essence, it acts as a safeguard for the lender, ensuring that they have a claim on the property if the borrower fails to repay the loan.

There are typically three parties involved in a Deed of Trust: the borrower (also known as the trustor), the lender (the beneficiary), and the trustee. The borrower is the person taking out the loan, the lender is the financial institution providing the loan, and the trustee is an impartial third party who holds the title until the loan is repaid.

When a borrower takes out a loan, they sign the Deed of Trust, which allows the lender to place a lien on the property. The borrower retains the right to live in and use the property, but if they default on the loan, the trustee can initiate foreclosure proceedings to sell the property and recover the loan amount. This process is often quicker than traditional mortgage foreclosures.

One significant advantage is the streamlined foreclosure process. In many states, a Deed of Trust allows for non-judicial foreclosure, meaning the lender can foreclose without going to court. This can save time and legal costs. Additionally, it provides clarity on the rights and responsibilities of all parties involved.

Yes, a Deed of Trust can be modified, but this typically requires agreement from all parties involved. If the borrower needs to change the terms of the loan, they should contact the lender to discuss possible modifications. It’s important to have any changes documented properly to ensure they are legally binding.

If the borrower defaults, the lender can instruct the trustee to begin foreclosure proceedings. The trustee will then sell the property to recover the outstanding loan amount. The process varies by state, so it’s essential for borrowers to understand the laws governing Deeds of Trust in their area.

No, while both a Deed of Trust and a mortgage serve similar purposes in securing a loan, they are different legal instruments. A mortgage involves only two parties—the borrower and the lender—while a Deed of Trust involves a third party, the trustee. The processes for foreclosure also differ between the two.

United States Tod - Consider the implications of this deed in your overall financial and estate planning.

When considering a Texas Quitclaim Deed, it's important to understand that this document serves to transfer ownership interest without the assurance of a clear title. This type of deed is often used informally, especially among family members, making it a convenient option for changing property ownership. For more detailed information on the process and legal implications, you can visit topformsonline.com/.

What Is a Deed in Lieu - It represents a proactive step a borrower can take to address their financial situation while minimizing foreclosure impact.

| Fact Name | Description |

|---|---|

| Definition | A Deed of Trust is a legal document used in real estate transactions to secure a loan. |

| Parties Involved | The document involves three parties: the borrower (trustor), the lender (beneficiary), and the trustee. |

| Purpose | It serves to transfer the legal title of the property to the trustee until the loan is paid off. |

| Foreclosure Process | In case of default, the trustee can initiate a non-judicial foreclosure process. |

| Governing Law | The Deed of Trust is governed by state law, which varies by jurisdiction. |

| Recording | The Deed of Trust must be recorded with the county recorder's office to be enforceable against third parties. |

| State-Specific Forms | Each state may have its own specific form and requirements for the Deed of Trust. |

| Right of Redemption | Some states allow borrowers a right of redemption after foreclosure, while others do not. |