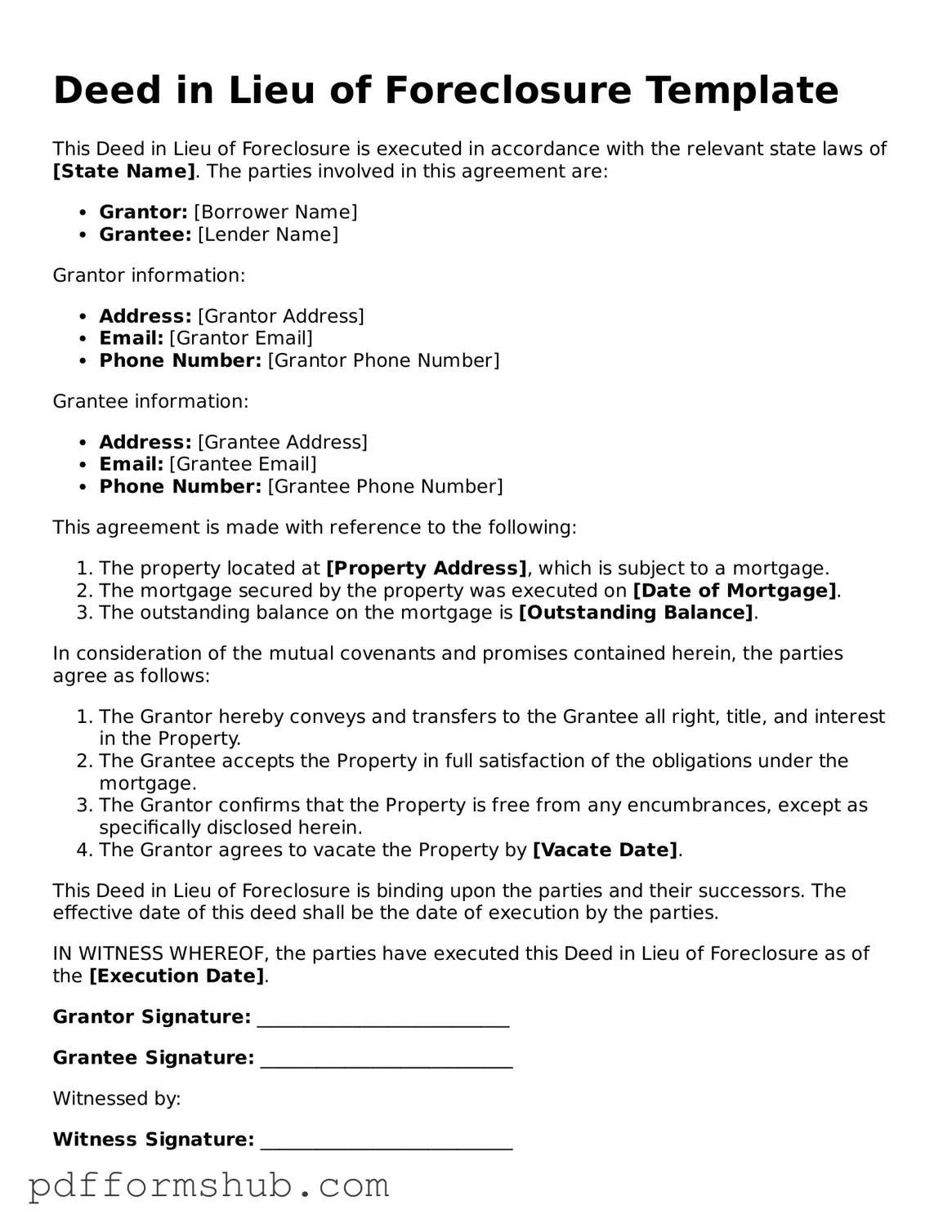

Valid Deed in Lieu of Foreclosure Form

PDF Forms Hub

Valid Deed in Lieu of Foreclosure Form

When facing the possibility of foreclosure, homeowners often seek alternatives to protect their financial future and minimize the impact on their credit. One such option is the Deed in Lieu of Foreclosure, a legal process that allows a homeowner to voluntarily transfer their property to the lender. This arrangement can help both parties avoid the lengthy and costly foreclosure process. By signing this document, the homeowner relinquishes their rights to the property, while the lender agrees to forgive the remaining mortgage debt. It’s important to note that this form may not be suitable for everyone, as it typically requires the homeowner to be in a position where they can no longer keep up with mortgage payments. Understanding the implications of a Deed in Lieu of Foreclosure is crucial, as it can impact credit scores and future home buying opportunities. However, for those who qualify, this option can provide a fresh start and relief from financial stress.

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to transfer ownership of their property to the lender to avoid foreclosure. This process often involves several additional forms and documents that facilitate the transaction. Below are some commonly used documents that accompany the Deed in Lieu of Foreclosure.

Understanding these documents is essential for both homeowners and lenders to ensure a smooth transition during the Deed in Lieu of Foreclosure process. Each document plays a crucial role in clarifying responsibilities and protecting the interests of all parties involved.

When considering a Deed in Lieu of Foreclosure, it's important to approach the process carefully. Here are five things to keep in mind while filling out the form:

By following these guidelines, you can help ensure that the process goes smoothly and that your rights are protected during this difficult time.

What is a Deed in Lieu of Foreclosure?

A Deed in Lieu of Foreclosure is a legal document that allows a homeowner to voluntarily transfer ownership of their property to the lender in order to avoid foreclosure. This process typically occurs when the homeowner is unable to keep up with mortgage payments and seeks an alternative to foreclosure proceedings.

How does a Deed in Lieu of Foreclosure work?

In this arrangement, the homeowner agrees to give the property back to the lender. In return, the lender often forgives the remaining mortgage debt. The homeowner must typically provide documentation of financial hardship and may need to meet specific criteria set by the lender.

What are the benefits of a Deed in Lieu of Foreclosure?

Are there any drawbacks to a Deed in Lieu of Foreclosure?

While there are benefits, there are also potential downsides. Homeowners may face tax implications, as forgiven debt can sometimes be considered taxable income. Additionally, not all lenders accept a Deed in Lieu, and the process can still impact credit ratings.

What steps should a homeowner take to initiate a Deed in Lieu of Foreclosure?

First, the homeowner should contact their lender to discuss their situation. Gathering financial documents, such as income statements and proof of hardship, is crucial. After that, the homeowner can formally request a Deed in Lieu and begin negotiations with the lender.

Will I still be responsible for my mortgage payments during this process?

Yes, homeowners are typically expected to continue making mortgage payments until the Deed in Lieu is finalized. This helps prevent further financial complications and demonstrates good faith to the lender.

Can I still apply for a mortgage in the future after completing a Deed in Lieu of Foreclosure?

Yes, it is possible to obtain a mortgage after a Deed in Lieu, but it may take time. Lenders will review your credit history and financial situation. Generally, waiting period requirements can vary, but it is often advisable to wait at least two to four years before applying for a new mortgage.

Gift Deed Form - A gift deed can have specific language to clarify intentions.

Correction Deed Form California - Use this form to correct previous errors that could hinder sales.

The California Vehicle Purchase Agreement is a legally binding document that outlines the terms and conditions between a buyer and a seller in a vehicle transaction. This form serves to protect the interests of both parties by detailing key elements such as the vehicle's price, condition, and any warranties involved. Understanding this agreement is essential for a smooth and transparent car buying experience in California, and you can find more information about it at https://topformsonline.com/.

Deed of Trust Template - A Deed of Trust is commonly used in real estate transactions across the U.S.

| Fact Name | Description |

|---|---|

| Definition | A Deed in Lieu of Foreclosure is an agreement where a homeowner voluntarily transfers property ownership to the lender to avoid foreclosure. |

| Benefits | This process can help homeowners avoid the lengthy foreclosure process and minimize damage to their credit score. |

| Requirements | Typically, homeowners must be behind on mortgage payments and unable to catch up to qualify for this option. |

| State Variations | Each state may have different laws governing the process. For example, California follows the California Civil Code Section 2929.5. |

| Tax Implications | Homeowners should be aware that the IRS may consider forgiven mortgage debt as taxable income. |

| Impact on Credit | While a Deed in Lieu of Foreclosure is less damaging than a foreclosure, it can still negatively affect a homeowner's credit score. |