Attorney-Verified Promissory Note Form for California State

PDF Forms Hub

Attorney-Verified Promissory Note Form for California State

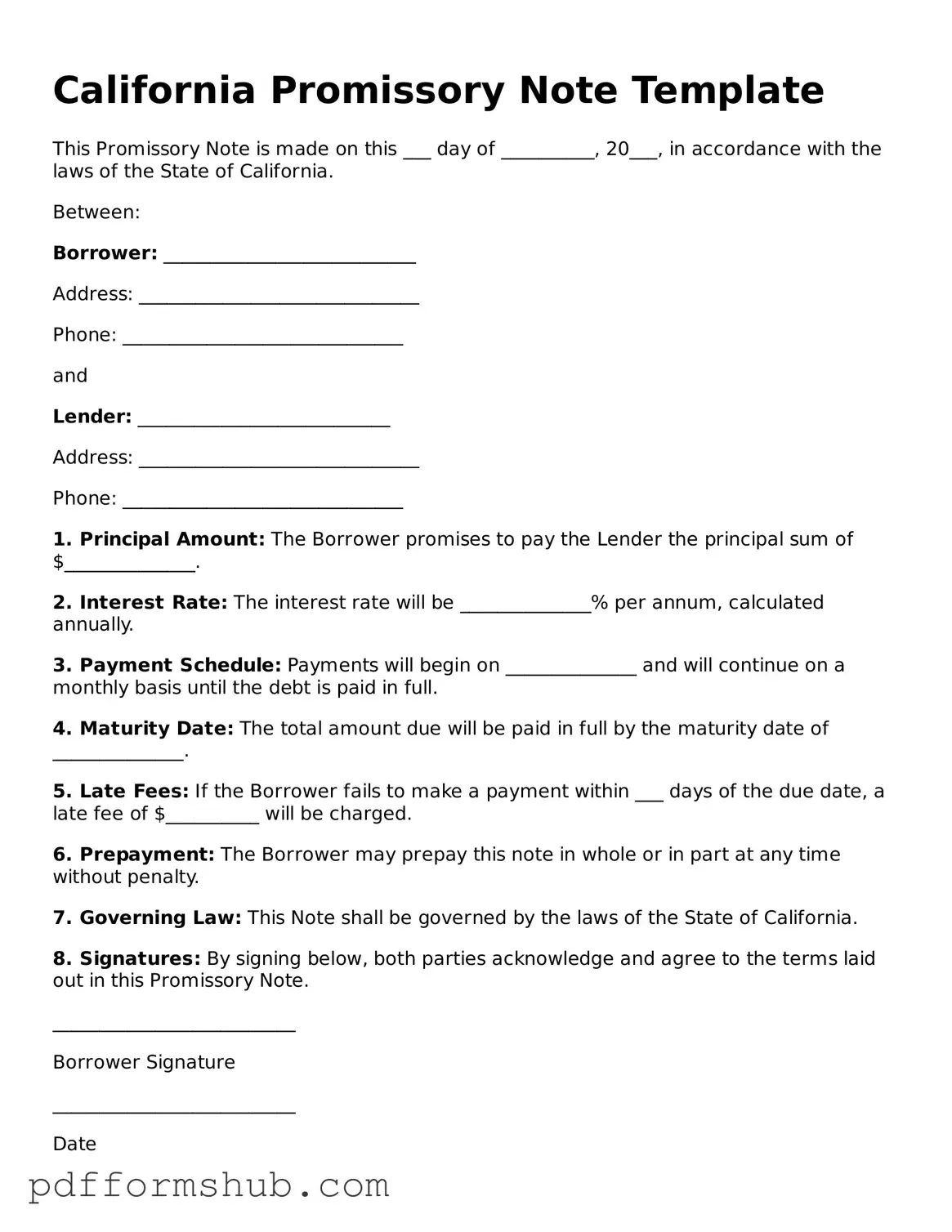

The California Promissory Note form serves as a crucial instrument in the realm of personal and commercial lending, encapsulating the terms of a loan agreement between a borrower and a lender. This legally binding document outlines essential components, such as the principal amount borrowed, the interest rate applicable, and the repayment schedule, thereby providing clarity and protection for both parties involved. Additionally, the form delineates the consequences of default, ensuring that the lender has recourse in the event of non-payment. Notably, it often includes provisions regarding prepayment options, which allow borrowers the flexibility to pay off their loans ahead of schedule without incurring penalties. Furthermore, the California Promissory Note may also specify whether the loan is secured or unsecured, influencing the level of risk for the lender and the terms of enforcement in case of default. By establishing clear expectations and responsibilities, this form not only facilitates the lending process but also fosters trust between the parties, making it an indispensable tool in financial transactions across the state.

When dealing with a California Promissory Note, several other forms and documents may accompany it to ensure clarity and legal compliance. Each of these documents plays a crucial role in the lending process, providing additional information and protections for both parties involved. Below is a list of commonly used forms that often accompany a Promissory Note.

Understanding these accompanying documents is essential for anyone involved in a lending arrangement. Each form serves a specific purpose, contributing to a well-structured and legally sound transaction. By ensuring all necessary documentation is in place, both lenders and borrowers can protect their interests and facilitate a smoother lending process.

When filling out a California Promissory Note form, it is essential to approach the task with care and attention to detail. Below is a list of things you should and shouldn't do to ensure the document is completed correctly.

By following these guidelines, you can help ensure that your California Promissory Note is properly executed and legally binding.

A California Promissory Note is a legal document in which one party (the borrower) agrees to pay a specific amount of money to another party (the lender) under agreed-upon terms. This document outlines the repayment schedule, interest rate, and any consequences for defaulting on the loan.

The main components of a California Promissory Note include:

Yes, a properly executed Promissory Note is a legally binding contract. Once signed by both parties, it creates an obligation for the borrower to repay the loan according to the specified terms. In the event of non-payment, the lender has the right to take legal action to recover the owed amount.

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A lawyer can ensure that the document complies with California laws and adequately protects the interests of both parties. However, many templates are available for those who choose to draft their own notes.

Yes, a Promissory Note can be modified if both the borrower and lender agree to the changes. Modifications should be documented in writing and signed by both parties to maintain clarity and legal enforceability. It is advisable to outline the specific changes and retain a copy of the modified agreement.

If the borrower defaults on the loan, the lender may take several actions, depending on the terms outlined in the Promissory Note. These actions can include charging late fees, accelerating the loan (demanding full repayment), or pursuing legal action to recover the owed amount. The specific remedies available will depend on the language of the note and applicable state laws.

Illinois Promissory Note - Adjustments to the terms of a promissory note may require mutual consent from both parties.

Florida Promissory Note Requirements - Understanding the implications of a promissory note can help protect both lenders and borrowers from potential pitfalls.

Creating a comprehensive Last Will and Testament is crucial for anyone wanting to secure their legacy and ensure that their wishes are respected. For those looking for assistance in drafting this important document, Templates and Guide can provide valuable resources and examples to simplify the process and avoid potential conflicts among loved ones.

Georgia Promissory Note - The document should be filled out completely to avoid future complications.

| Fact Name | Description |

|---|---|

| Definition | A California Promissory Note is a written promise to pay a specific amount of money to a designated person or entity at a specified time. |

| Governing Law | The California Civil Code, specifically Sections 3300-3352, governs promissory notes in California. |

| Parties Involved | Typically, there are two main parties: the borrower (maker) who promises to pay, and the lender (payee) who receives the payment. |

| Interest Rate | The note can specify an interest rate, which must comply with California usury laws to avoid excessive charges. |

| Repayment Terms | Repayment terms, including the payment schedule and due dates, should be clearly outlined in the note. |

| Default Clauses | Default provisions can be included, detailing what happens if the borrower fails to make payments as agreed. |

| Notarization | While notarization is not always required, having the note notarized can provide additional legal protection and authenticity. |

| Transferability | A promissory note can often be sold or transferred to another party, allowing for flexibility in financial arrangements. |